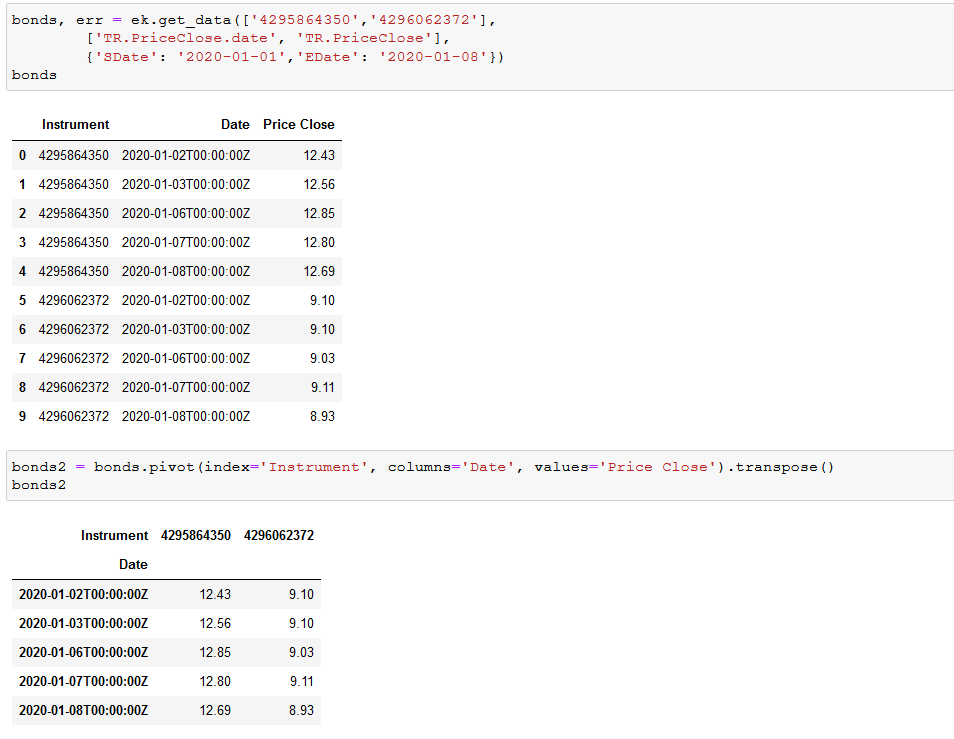

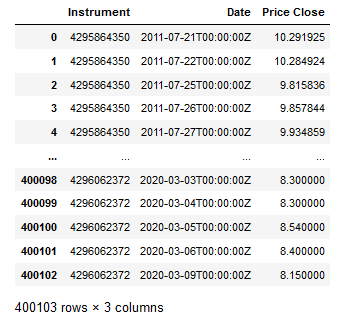

I need to estimate CAR for a bunch of bonds issuers, so I am starting by getting their closing price. I am unable to resample with a single index and get the data on different columns.

bonds, err = ek.get_data(

df['Ultimate Parent ID'],

['TR.PriceClose.date', 'TR.PriceClose'],

{'SDate': '2020-01-01',

'EDate': '2020-10-01'})

What I get is:

I would prefer to get a single timeseries with a column for each instrument, but I am unable to rearrange the df. Should I use ek.get_timeseries instead?